The costs for material and conversion need to reconcile with the total beginning inventory and the costs incurred for the department during that month. The equivalent unit calculations are carried forward into the “cost per equivalent unit” schedule. This shows how the combined costs from beginning work in process (assumed at $2,122,500) and current period production (assumed at $7,365,000) are divided by the equivalent units. The result is the weighted-average cost per equivalent unit for each factor of production. The individual cost factors can be combined to identify conversion cost and overall cost per equivalent unit.

Formula for Equivalent Units of Production

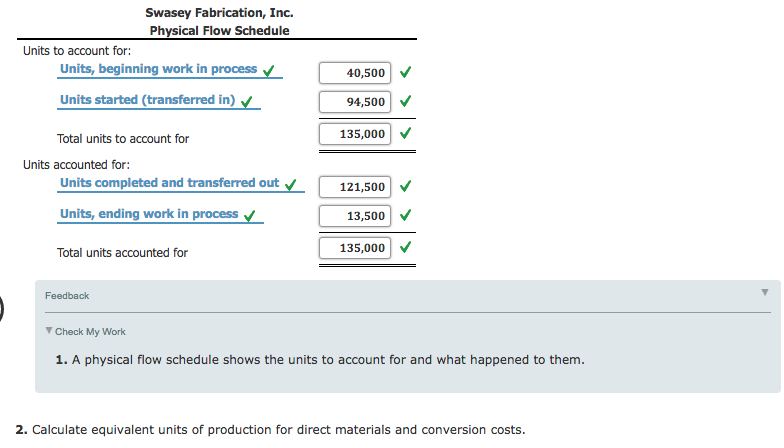

Determining the value of the work in process inventory accounts is challenging because each product is at varying stages of completion and the computation needs to be done for each department. Trying to determine the value of those partial stages of completion requires application of the equivalent unit computation. The equivalent unit computation determines the number of units if each is manufactured in its entirety before manufacturing the next unit. For example, forty units that are 25% complete would be ten (40 × 25%) units that are totally complete. Obviously the units started and completed during the period are 100% complete and the equivalent units are the same as the physical units. The beginning WIP units are already partially complete at the start of the period and are further completed during the period and need to be converted to equivalent units.

- During the accounting period a further 8,000 units are added to the production process and 6,000 units are completed and transferred out, leaving an ending balance of 4,000 units in work in process.

- You apply costs by multiplying the rates for direct materials, conversion costs, and transferred-in cost by (1) ending WIP equivalent units and (2) completed units.

- Direct material is added in stages, such as the beginning, middle, or end of the process, while conversion costs are expensed evenly over the process.

- Process costing firms usually have several departments that products must pass through before they’re complete.

- Some overhead cost should go to these units still in WIP, just not a full unit’s worth of overhead costs.

Create a Free Account and Ask Any Financial Question

Compare the subtractive method (see above figure in Section 6.5.2) to the additive method (below). The Units Completed term we’ve used already excludes any ending WIP units, so we just need to subtract away those units in beginning WIP. This video will provide a demonstration of cost assignment under the FIFO method.

Which of these is most important for your financial advisor to have?

Let’s assume a unit in ending WIP is about halfway through the process of completion. It would be natural to assume it is about 50% complete (and thus equal to 0.5 equivalent units). To measure output accurately, these partially completed units must be considered in the output computation.

Cost Per Equivalent Unit

Ending work in process is 1/3 complete for conversion costs, but what about materials? The weighted average method rips away the $15,000 of conversion costs from the beginning WIP units. It treats those $15,000 as if they were incurred this period (even though we know they were incurred last period, otherwise they wouldn’t be the beginning WIP balance). This means those $15,000 of conversion costs end up redistributed across all equivalent salaries payable definition and meaning units worked on this period because they’re included in the conversion cost per equivalent unit rate we just calculated. The units in beginning WIP are effectively treated as if they had no work done on them at all in the prior period, and they are lumped in with all the other units completed this period. In addition to the equivalent units, it is necessary to track the units completed as well as the units remaining in ending inventory.

Equivalent Units FIFO method

These costs are then used to calculate the equivalent units and total production costs in a four-step process. I explained, above, FIFO’s Step #3 using what’s called the subtractive method. I told you to subtract the beginning WIP equivalent units from the total units completed so we could apply the rates to the equivalent units completed using this period’s work. Process costing firms usually have several departments that products must pass through before they’re complete. For responsibility accounting purposes these departments costs should be kept separate. So each department allocates costs at the end of the period to reflect the units that department completed and transferred onward to the next department.

Our writing and editorial staff are a team of experts holding advanced financial designations and have written for most major financial media publications. Our work has been directly cited by organizations including Entrepreneur, Business Insider, Investopedia, Forbes, CNBC, and many others. For information pertaining to the registration status of 11 Financial, please contact the state securities regulators for those states in which 11 Financial maintains a registration filing. Double Entry Bookkeeping is here to provide you with free online information to help you learn and understand bookkeeping and introductory accounting.

Forunits in ending work in process, we would take the units unfinishedx a percent complete. The percent complete can be different fordirect materials, direct labor or overhead. For the shaping department, the materials are 100% complete with regard to materials costs and 35% complete with regard to conversion costs. The 7,500 units completed and transferred out to the finishing department must be 100% complete with regard to materials and conversion, so they make up 7,500 (7,500 × 100%) units.

Since the maximum number of units that could possibly be completed is 8,700, the number of units in the shaping department’s ending inventory must be 1,200. The total of the 7,500 units completed and transferred out and the 1,200 units in ending inventory equal the 8,700 possible units in the shaping department. Equivalent units FIFO method is used by a manufacturer to express partially completed units of product in terms of finished units.

If all the product units are the same, each product unit is probably responsible for the same amount of overhead cost. To spend time or money on deciding each unit’s responsibility for overhead costs down to the micro-penny is a waste. If the closing work-in-progress is 800 units, 70% complete in all respects, the equivalent units of production of closing work-in-progress is 560 units (i.e., 800 x 70%). Essentially, the concept ofequivalentunits involves expressing a given number ofpartially completed units as a smaller number of fully completedunits. We do this because it is easier to account for whole unitsthen parts of a unit. We are adding together partially completedunits to make a whole unit.

Neueste Kommentare